April 28, 2021

Article

We often see farming businesses short of cash and refinancing existing borrowings over a longer term to help cash flow. For most cases, this is because the original borrowing was taken out over too short a term.

When taking new borrowing, it is important to consider the appropriate borrowing terms for both the asset being purchased, or invested in, and the business.

It is often the case that the asset purchased and financed suits a longer term of lending and, if financed on shorter terms, the business cannot afford the repayments after considering other areas of reinvestment that are needed for the business.

Where borrowing is taken out over too short a term it often results in the business increasing its overdraft or having to fund more machinery reinvestment on hire purchase agreements. Hire purchase agreements often make this problem worse as the monthly cash commitments continue to degenerate cash flow.

Example

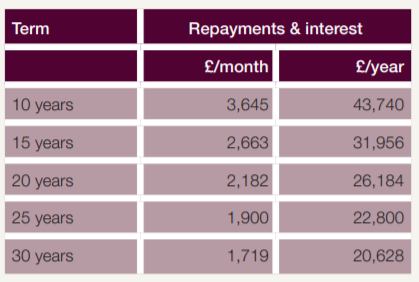

Tom Stone Farming is purchasing an additional 45 acres of farmland for £360,000. This land is usually rented each year. Therefore, there will only be a minimal rent saving to each year of approximately £6,500.

The business doesn’t have any cash to buy the land and is therefore considering its options for financing the land

on a commercial loan. The bank has come back with the following options for the business:

If we consider the how long the term of the funding should be based on the asset and business:

1. The asset

The asset is farmland. Farmland would suit longer term lending as it’s life is infinite. Farmland historically has always risen in value and therefore long term borrowing shouldn’t affect the residual value. This would mean that the based on the asset the lending should be 20 years and over.

2. The business

We do not know the profitability of the business but on the basis that the bank is offering all lending terms then we

can assume it is very profitable and does generate a cash surplus each year. However, the business has no cash to

invest in the land and therefore we must assume that the cash surplus is being reinvested in growing the business.

With the land purchase only resulting in a cash saving of £6,500 of rent then the majority of the cash for the repayments will need to come from the existing business. The business would therefore suit a longer term of 20-30 years.

In summary, the new borrowing should be on a term of at least 20 years.

Instead, we might see businesses making the decision to repay the debt over 10 or 15 years. Each of these terms, when being compared to say a 25 year term, would adversely affect cash by an extra £1,745/month (£20,940/year) or £763/month (£9,156/year).

The barrier to taking a longer term is often the extra interest payable. However, it is important to remember that you will get tax relief on the additional interest and with fixed interest rates are currently very low. You should back your business to gain you a better return on the initial cash flow savings of the longer term rather than repaying a loan quickly and having less cash to reinvest in the business.

View the full copy of our spring edition of Rural Intelligence for Farms & Estates here.