October 06, 2021

Article

Organisations with a turnover in excess of £10.2 million, who are within the remit of anti-money laundering (AML) legislation, will see the cost of regulation increase in 2023/24 with the introduction of a new Economic Crime Levy, which is due to be legislated for via the Finance Bill later this Autumn.

The levy is expected to raise £100 million a year from 2023/24 onwards. To ensure that there is both transparency and accountability around the levy, an annual report will be produced setting out the levy’s operation, with a further wide ranging review being planned before the end of 2027.

When will the first levy be charged?

The levy will be charged based on the “relevant accounting period” ending in the “levy year”.

The “levy year” is

- the period of 12 months beginning with 1 April 2022, and

- each subsequent period of 12 months.

The “relevant accounting period” is the accounting period of the entity which ends within the levy year.

On this basis an organisation with a 31 March accounting period will first be subject to levy for the year ended 31 March 2023 and an organisation with a 31 December accounting period will first apply the levy to the year ended 31 December 2022.

The government have set out that the first payments of the levy will then be made during the year 1 April 2023 to 31 March 2024.

How will the levy be calculated?

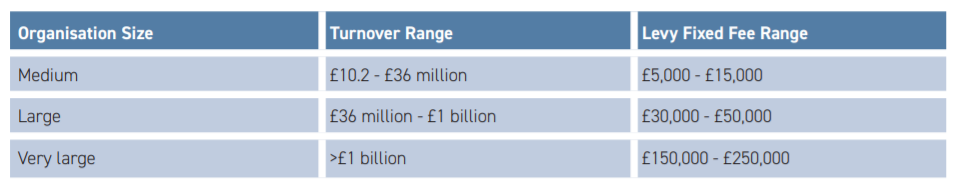

The levy will be paid as a fixed fee based on the level of UK revenue for the relevant accounting period. Small organisations with a turnover of less than £10.2 million will be exempt. The potential ranges of levy for other organisations have been set out in the government response document and are summarised as follows:

Working on the basis of the bigger the entity, the higher the levy, the fixed ranges above should give organisations an idea as to how much their levy payment may be based on the draft legislation. The final fixed fees will be specified in the Finance Bill when it is introduced.

Who will collect the levy?

The FCA, HMRC, and the Gambling Commission (GC), will collect the levy from their own AML-supervised populations, with HMRC also collecting the levy for the entities supervised by the 22 legal and accountancy Professional Body Supervisors.