March 25, 2021

Article

Case Study

Mr & Mrs x had been offered £6million for their successful business. They wanted to know if this offer would enable them to meet their short-term objectives and support them for the remainder of their lives. Whilst they appreciated that £6million was a large figure, they were only 54 and 52 years of age and had no idea as the longevity of this value. Therefore, they required a cash flow plan.

Mr & Mrs X wanted to achieve the following in the short and longer term:

- Pay off all existing mortgages on day one and complete renovations on their main residence.

- Gift a total of £1.5million to family on day one.

- Annual Expenditure of £200,000 per annum until they attain age 70.*

- From age 70, the annual expenditure would reduce down to £150,000 per annum.*

- At age 70, a further cash injection of £500,000 from proposed downsize.

*Expenditure assumed to increase by inflation (2.5%) per annum.

In addition to the proceeds of the business sale, the clients existing assets were also incorporate into the cash flow model to give a full overview. These assets included pension funds and a buy to let property.

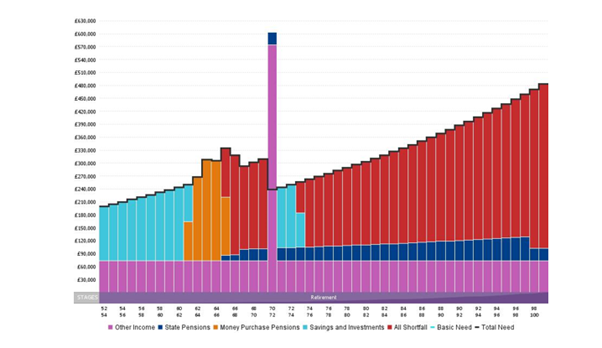

The result of this cash flow is displayed below:

After analysing the full situation, we were able to confirm that the offer of £6million would not be sufficient to meet their objectives. The business proceeds were able to meet the short-term objectives but would be exhausted by age 61. At this point we were able to identify that the pension funds could then be used to provide an income, but they would also be exhausted by age 65. This means that Mr & Mrs X would not be able to sustain their required standard of living if they accepted the offer of £6 million.

Having understood the position, the clients were extremely grateful for the service and wondered if we could work backwards to work out the optimum sale price. This would allow them to see what offer they could accept and meet their objectives.

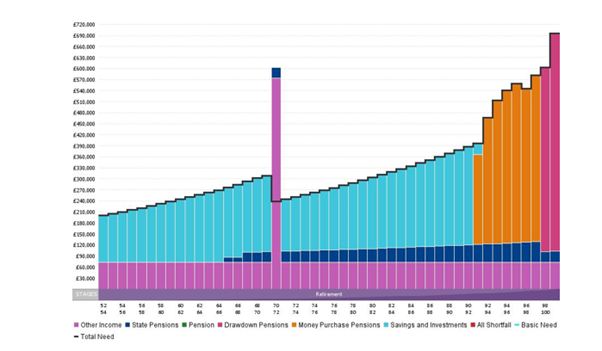

Having ran through various scenarios, we were able to determine that the optimum sale price would be £10million. The key factor that the clients found extremely useful was that the cash flow forecasts can be completed ‘live’ with the clients present. This allowed the clients to make minor amendments throughout the process.

The forecast below confirms that the £10million would allow them to meet all of their objectives and have an inflation adjusted income for life.

Summary

Whilst the cash flow is simply a projection of a scenario, it gave the clients comfort if knowing that the offer they received was not sufficient for their needs. They were unlikely to be able to counter the offer up to the level of required assets, but it allowed them to show evidence as to why they would not accept that offer.

Cash flows are extremely important for anyone that is going through a change in circumstances. As well as business sales, cash flows are extremely useful for individual approaching retirement that want to understand the longevity of their pension assets.

If you would like to discuss a cash flow plan of your own, please get in touch and I will be happy to discuss this in more detail.

*Albert Goodman Chartered Financial Planners is the trading style of Albert Goodman Financial Planning Ltd, which is authorised and regulated by the Financial Conduct Authority. The Financial Conduct Authority does not regulate inheritance tax planning.